Science based target setting: The Methods

We review the approaches to setting Science Based Targets (SBTs). How do we act on the warning signs with a viable and truly science-based approach?

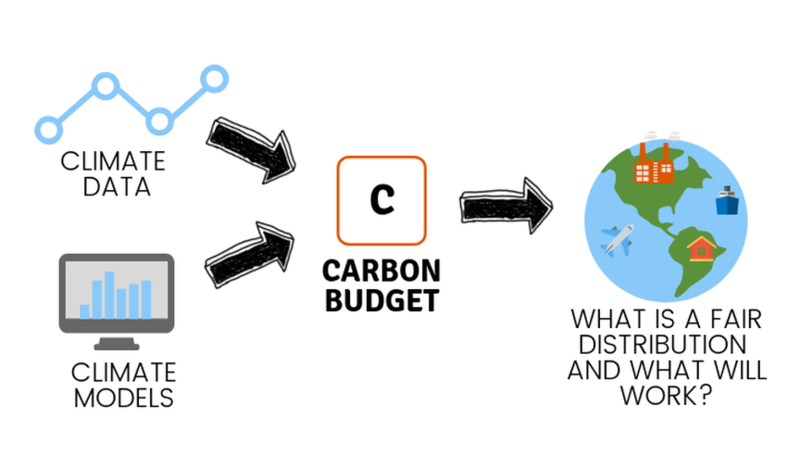

The Science based target approach- turning signals into solutions

The basis of the science-based target (SBT) approach is easily understood:

- Climate data show the historic impacts of emitting certain levels of greenhouse gases into the atmosphere.

- Climate models use this data to predict the impacts of further emissions.

- Once we have agreed on an acceptable warming scenario and degree of probability, we calculate how much carbon can safely be emitted, and when this can occur. We call this our ‘carbon budget'.

- This budget is distributed acorss nations, industrial sectors or companies depending on the method employed.

But how do we determine a basis for sharing out this budget which is fair, measurable and workable? Should we divide the budget between nations, or, given our globalised world, between industrial sectors? How do we deal with diffuse and carbon-intensive industries such as international aviation? Should we apply the ‘polluter pays’ principle and penalise countries with the largest historical emissions?

The Science-based Targets Initiative

Recognising the need, a coalition of organisations came together in 2013 to form the Science-based Targets Initiative (SBTi), including CDP, the United Nations Global Compact (UNGC), the World Resources Institute (WRI), and the WWF. The SBTi has assumed a role of central authority on science-driven carbon targets, providing a free ‘target review’ service and publically recognising SBT efforts of businesses.

Three general approaches to setting SBTs

The SBTi recognise three general approaches to setting SBTs.

1. Sector-based approach: This is the approach taken in the SBTI’s own methodology: the Sectoral Decarbonisation Approach (SDA). In this approach the carbon budget for the global economy is divided into 13 sub-sectors. These include six of the most carbon-intensive industrial activities (Power Generation, Cement, Iron and Steel, Aluminium, Chemical and Petrochemicals and Pulp and Paper), four transport sub-sectors (heavy-duty and light-duty road travel, rail passenger and aviation) and a sub-sector to cover Service Buildings (all kinds of non-domestic building). Two further sectors act as a ‘catch-all’ for the remainder of the world economy.

Each sub-sector is allocated an ‘activity denominator’ which measures the level of economic activity and enables a carbon intensity pathway to 2050 to be calculated (looking at scope 1 and 2 emissions). For homogenous sub-sectors such as cement or aluminium this is simply tonnes of product. For more heterogeneous sectors the choice of activity metric is more challenging – for Service Buildings ‘floor area’ is used. This simplification introduces the first potential weakness of this method – clearly the carbon intensity per unit floor area of a hospital, an office and a restaurant are potentially very different. The 2050 pathways are designed to account for any projected growth or shrinkage in each sector. Company carbon targets are judged to be ‘science-based’ if they comply with the decarbonisation pathway for their sector.

This approach has further weaknesses. In seeking to develop a global benchmark for decarbonisation, the more developed economies of the world are essentially let ‘off the hook’ as they are already some distance along the road. Should economies like the UK and Germany work to a more carbon-constrained target given their increased prosperity and advanced decarbonisation programmes in contrast with say, India and China?

2. Absolute contraction approach. In this approach, companies are assigned the same percentage of absolute emission reductions as is required globally. While simple and clear, this is arguably crude: it does not recognise early action and misses the opportunity to assign greater decarbonisation in companies where abatement might be cheaper or more feasible. It also does not address company growth/decline - a company losing market share at a rate higher than the global economic growth projections in the scenario is permitted to increase its emissions intensity. Finally, it does not take account of the potentially large variability of abatement costs across sectors.

3. Economic based approaches (such as ‘Greenhouse Gas Emissions per unit of Value Added’, or GEVA) have their own limitations. Like the contraction methods, they do not consider differences in abatement costs across sectors. Furthermore, they do not address the impact of exchange rates, an issue which has been identified as significant in a number of CDP submissions. Could this be addressed with Purchasing power parity (PPP), a method which allows one to estimate what the exchange rate between two currencies would have to be in order for the exchange to be at par with the purchasing power of the two countries' currencies. Finally, they do not address the ‘premiumisation’ of products simply based on higher spend on marketing (which would reduce value added intensity without the need to reduce operational emissions). The choice of approach will depend on the type of business and the products or services it sells. We advise businesses to first consider the Sector Decarbonisation Approach and Absolute Emission Contraction approach, as these are recommended by the SBTI.

Our advice

Whichever method is chosen, we advise businesses to look beyond simply complying with an SBT pathway. In our recent thought-piece jointly authored with Hillbreak and our recent animation entitled ‘The Climate Coin Toss’, we outlined the reasons why we do not believe that the SBTi targets are strong or ambitious enough. Chief of these is that fact that the decarbonisation pathways underpinning the SBTi’s methods are based on a 50% likelihood of restricting global average temperature rise to 2°C – essentially a ‘coin toss’ chance of avoiding climate breakdown. Another key weakness is the potential ‘race to the bottom’ that might be started. If all business sustainability leaders adopt targets based on a global sector average, the chances of those sector pathways being realised become very small.

Multiple business benefits from taking this approach

We believe that businesses can and should go further than the SBT pathway. As well as benefitting the planet, there is strong commercial value in doing so:

- Significant cost savings: through more efficient use of resources

- Risk mitigation: by reducing carbon intensity of your operations

- Supply chain collaboration and innovation: by working more closely with suppliers and customers to cut carbon

- Business and brand reputation: a strong target can reinforce a brand for increasingly climate-conscious consumers, and investors.

- A forward-looking approach: there is a growing focus among business on the ‘route to net zero’, particularly in the real estate sector. We will explore this further in the next thought-piece.