Science Based Targets initiative – Buildings Guidance Consultation

On the 16th May 2023, the SBTi published their long-awaited Buildings Guidance for consultation. Building off CRREM V2 and research conducted by Ramboll, the guidance offers a decoupled approach to target setting for addressing in-use emissions as well as upfront embodied carbon emissions associated with the built environment. The guidance also provides building specific clarity for more ambiguous areas of the GHG Protocol, addressing several nuances in the target setting process to account for the unique nature of the built environment as an economic sector.

The guidance document and underlying methodology for the upfront embodied carbon targets are currently open for public consultation, requiring feedback by the 16th July.

The key headlines of the proposed update are:

The use of actual target values is a deviation in methodology for the SBTi, which typically focuses on percentage reductions from a baseline value.

In-use (operational) emissions targets are based on the CRREM V2 carbon targets and therefore provided on a specific basis for over 40 countries and 12 property types.

Embodied emissions targets only cover upfront emissions [A1-A5] for newly constructed buildings only and are only provided for three specific property types, (offices, residential and retail) with all others being classified as ‘other’.

Targets to be set on other corporate emission sources (e.g. purchased goods and services required to operate a building) are to be developed in line with the guidance in the Corporate Standard.

An additional target required by the SBTi is for users not to install any new fossil fuel heating/cooking systems from 2025.

While the guidance provides a series of useful guidelines in recognition of the requirements of the built environment, and a significant focus on immediate emissions reduction, too many questions have been left unanswered and gaps in the approach still exist.

The consultation is explored in greater detail below.

What is the Science Based Targets initiative (SBTi)?

The Science Based Targets initiative (SBTi) is a partnership between CDP, the UN Global Compact, WRI and the WWF, providing methodologies for businesses to set decarbonisation targets that are considered ‘science-based’ i.e., in line with the rate of decarbonisation under the Paris Agreement (2015) to limit average global heating to a maximum of 1.5°C above pre-industrial levels. Since the initiative’s launch, their methodology and validation of submissions has gained traction as one of the most robust set of emissions reduction targets available. Almost 2,700 companies (covering over a third of the global economy’s market capitalisation) have now set Science-based Targets.

The SBTi offer a range of methodologies for corporate target setting and are gradually developing their roster of sector-specific guidance. A crucial principle of the SBTi targets is that they must be achieved through actual emissions reductions (with the exception of the Portfolio Coverage and Temperature Rating methodologies for financial institutions) – there is no allowance for offsetting to contribute to achieving the reduction target.

While well regarded by many, the SBTi has recently been challenged by some for their lack of third party assurance or requirements for detailed strategies for achieving targets. Nevertheless, it remains one of the best available tools for setting corporate decarbonisation targets and they are currently developing a measuring, reporting and verification standard to begin addressing these concerns.

The Buildings Guidance

The built environment accounts for over a third of global emissions and the physical size of the global sector is expected to increase by 75% between 2020 and 2050. Recognising this significant impact and the unique nature of the sector, the SBTi kicked off the development of the Buildings Guidance in October 2021, with the aim of providing a 1.5°C target setting protocol for buildings. To achieve this across a whole building life cycle and value chain, the approach has been split into three focus-points, each with specific nuances to account for the unique nature of the sector:

Companies operating in the buildings sector (developers, owners/managers, occupiers with control and even design engineers/architects) must now adhere to this target-setting structure, providing proof if in-use or upfront embodied emissions are not relevant to their value chain.

The guidance provides a breakdown of the requirements of in-use and upfront embodied emissions targets related to buildings. Targets to be set on other corporate emission sources (e.g. purchased goods and services required to operate a building) are to be developed in line with the guidance in the Corporate Standard.

The in-use and upfront embodied emissions targets are provided as a set of discrete, normalised targets representing a large methodological change for the SBTi, which typically require more generalised reduction percentages from a baseline value. This methodological change provides organisations with much less accommodation for high emissions baselines and will therefore require a more immediate, proactive approach to achieving reductions.

The targets are specific to the building types within a portfolio and (for the in-use pathway) the property location. However, the options are not exhaustive of property types and locations, and more generalised targets are provided for each pathway to account for those that are not currently covered within the tool:

Table 1: Coverage of Property Types within the Buildings Guidance+

In-Use Emissions

GHG Accounting

For the purposes of in-use GHG emissions accounting, the SBTi directs users to the GHG Protocol for general guidelines, with a few additional requirements:

A location-based method must be used to ensure energy reduction is prioritised;

Companies must include f-gas emissions from all building types within their boundaries (baseline and targets). Where actual data is unavailable, an estimate must be used and the estimation methodology clearly disclosed; and

Normalisation to account for partial occupancy is recommended (but not required), using the ‘average annual vacancy’ of a property.

While this provides greater clarity for the sector, the SBTi fail to provide clarification on how an organisation might make adjustments for occupancy and intensity of use in specific assets when gap filling or setting targets. They also appear to contradict their location-based requirement in the below statement (pg 49):

“Targets to actively source renewable electricity at a rate that is consistent with 1.5°C scenarios are an acceptable alternative to scope 2 emission reduction targets.”

Additionally, reliance on location-based methods of accounting raises concerns for locations with carbon intensive grids.

Targets – CRREM

The Carbon Risk Real Estate Monitor (CRREM) is an EU-funded tool, primarily for the use of asset managers and investors, to identify the operational carbon stranding risk of buildings:

A ‘stranded asset’ has been defined by CRREM as a property that will not meet future carbon and energy efficiency standards and market expectations, and might be increasingly exposed to the risk of early economic obsolescence. CRREM sets the boundaries for the term ‘stranded’ based on the operational energy use of a building.

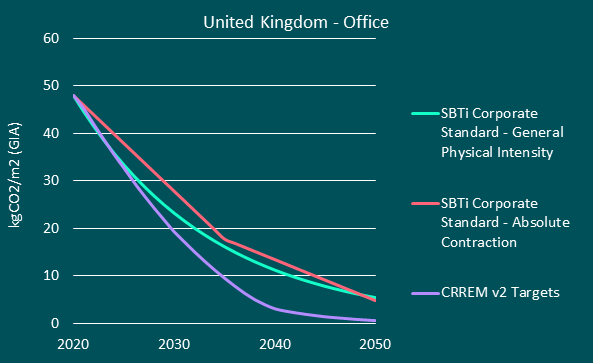

CRREM provides building-specific pathway targets on carbon and energy bases for 12 property types across 40 countries. Since the release of v1 of the tool in 2020, the targets have become widely recognised within the real estate industry as the most inclusive set of carbon descent targets available. CRREM have now partnered with the SBTi and released a second version of their pathways at the beginning of this year. The SBTi requires real estate organisations to use these targets for setting in-use emissions and they have developed a tool which aggregates CRREM targets for all location and property type combinations within a portfolio. While this provides users with a single, easily communicable target, it does also mean that the target is based on a weighted average reduction across the portfolio. This may lead to certain well-performing, low-risk assets skewing the apparent reductions achieved by a portfolio, allowing for more carbon-intensive assets to be somewhat left by the wayside.

In terms of the impact of this transition on property owners, managers and occupiers with existing SBTs, the CRREM pathways are typically more stringent in the long term than the requirements of the Corporate Standard for Scopes 1, 2 and 3 combined. A greater focus must therefore be applied to the reduction of Scope 3 emissions (the CRREM pathways are relatively well aligned with the Scope 1 and 2 reduction requirements already provided by the SDA). The below graph, shows this comparison between the percentage reductions from a baseline proposed by the Corporate Standard and the requirements of CRREM. For illustrative purposes, the starting baseline has been used as the CRREM 2020 value for each:

Figure 1: Comparison of SBTi Reduction Requirements

Note: While the SBTi tool uses the CRREM carbon targets, they recommend also using the energy targets to further enhance the robustness of climate risk management strategies.

Upfront Embodied Carbon Emissions

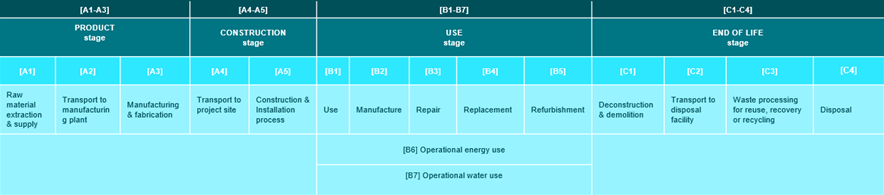

The SBTi have developed a 1.5°C -aligned emissions intensity pathway, in collaboration with Ramboll, for the upfront embodied carbon of newly constructed buildings, allowing users to set targets on their upfront embodied emissions at a portfolio or corporate level. These targets cover life cycle stages [A1 – A5]; the production and construction stages of the whole life carbon of the building, as outlined in Figure 2. The reason that the SBTi cite for excluding further emissions from use stages and end-of-life is that they are challenging to quantify and have a lack of availability in disaggregated data for different property types.

While the guidance defines the life cycle stages to be covered by the targets, it does not make it clear which building elements should be included within the scope e.g. are furnishings, fittings, and equipment (FFE) in scope of the upfront embodied carbon targets?

Figure 2: Modular information for the life cycle assessment as per EN 15978

The SBTi pathways for upfront embodied carbon emissions are currently only provided at a global level, but with the caveat that this may be expanded to sub-geographies in the future. The pathways are based on an academic research paper published in 2020, which presented the embodied carbon of ~230 buildings for different energy performance classes, property types, and geographies. Arguably, the UK already has improved it’s embodied carbon database since then, which is being collated in the Built Environment Carbon Database by a number of industry bodies, including BRE, CIBSE, UKGBC, RICs and others.

Who the SBTi recommend should set an upfront emissions target for new buildings?

Developers: treating new buildings as ‘capital goods’ and all emissions related to the construction of the building must be included in scope at practical completion.

The first owner/purchaser of a new building: upon practical completion

Entities/Financial Institutions which finance the construction, or first purchase of a new building– defining responsibility here is likely to be tricky!

Franchisors: optional

Manufacturers of construction materials are not expected to use the Buildings Sector Guidance and SDA, and should follow the relevant approach for their sector, e.g. the SBTi cement and steel guidance.

How can users set a target?

The SBTi has developed upfront embodied carbon pathways for 4 building types, residential, office, retail, and other. Where a building is mixed use, then the building type should be chosen for the highest share of the floor area. This approach may become complex for buildings with more mixed uses, leading to targets which may either be too challenging or easy to achieve.

What do the targets look like?

Figure 3: Comparison of Upfront Embodied Carbon Targets out to 2030

The charts, produced by BIP.Verco, show the SBTi upfront carbon intensity targets compared with LETI & GLA targets – you can see that they are closely aligned in 2025 and 2030. We would welcome more granular targets for different building types, e.g. the upfront carbon intensity of a high-rise apartment block is likely to be much higher than that of a 2-bed mid-terrace house, and recognition across geographies to more accurately reflect development practice and supply chains.

Built Environment Specific Considerations

As well as the above approaches to target setting, the SBTi have further recognised the unique needs of the buildings sector through a selection of provisions and clarifications on their interpretation of the GHG Protocol. Initially, a series of specifications are provided for GHG accounting and reporting in real estate:

Scope 3 Category 11 (Use of Sold Products) requires a minimum 60-year lifetime estimate to ensure a sufficient consideration of the lifetime emissions are considered (with emissions allocated to the year of sale).

A two-year grace period following the acquisition of existing (standing) buildings will be allowed before the asset is required to be included within GHG inventory/target boundaries. This will provide the reporting organisation with time to conduct any energy efficiency measures and changes to the fit out, as well as time to collect a full year worth of actual data before the emissions are included within their target boundary.

Partial base year emissions – where assets enter the portfolio partway through the reporting year:

- If acquired to sell, the owner must include emissions proportional to the reporting year period that they held the asset.

- If acquired for occupancy/leasing, the owner must include emissions for the entire reporting year. No information is provided on how to effectively pro-rate the available data.

- This accommodation of partial base year emissions seems to contradict the two-year grace period outlined in the above point – a point of uncertainty that the SBTi will need to clearly address.

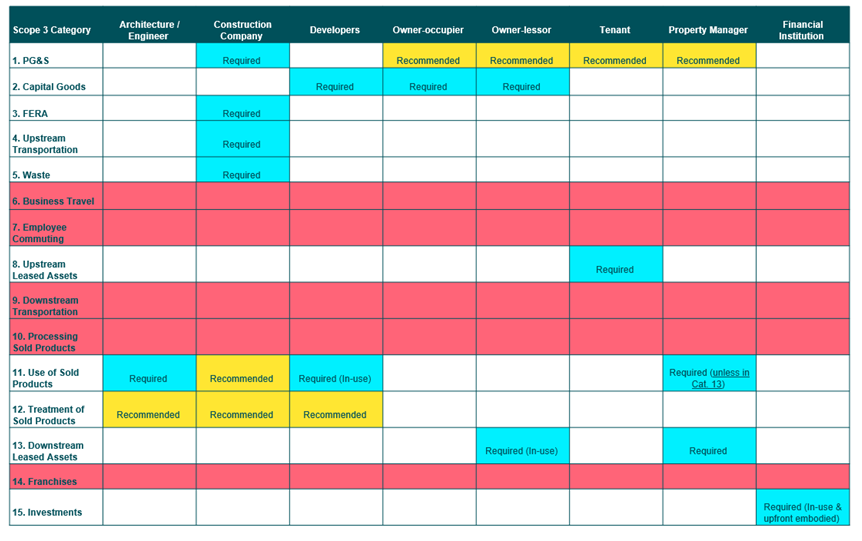

Specific inventory (and target) boundaries have been stipulated by the SBTi, based on the user, in recognition of the most material emissions sources within the built environment. Required Scope 3 categories must be included within target boundaries, even if Scope 3 emissions in total are below the usual SBTi inclusion threshold (< 40% of the total footprint). The below table outlines these requirements, as they relate to emissions scopes within the GHG inventory. However, note that the split of categories is not reflected in the in-use or upfront embodied carbon targets as these are set on a whole building basis. A few key takeaways from this breakdown are:

- Parties responsible for any upfront embodied carbon must include this within their targets (Category 11 for architects/engineers and Category 2 – Capital Goods – for developers and owners).

- Owner-occupiers are only required to include upfront embodied emissions within their Scope 3 boundary as their in-use emissions will fall under Scopes 1 and 2.

- Tenants must include Category 8 (Upstream leased assets) to avoid the exclusion of any in-use emissions.

Table 2: Overview of Required Categories by User Type

As well as these additional requirements for GHG accounting, the SBTi have outlined a series of additional guidelines on forward-looking target setting:

Organisations setting building targets must also publicly commit to no new installations of fossil fuel heating and cooking systems from 2025. However, no hard target is required on the removal of fossil fuel heating from existing buildings which is a key determiner of the pace of the low carbon transition.

The usual SBTi recalculation requirements for targets will also relate to building typology and geographical spread of a portfolio, not just organisational structure and activities. However, the requirement for recalculation is waived for Buildings Guidance Users that can demonstrate their business model is reliant on a high turnover of assets.

Similarly, the SBTi have adopted the term ‘Carbon Leakage’ to refer to emissions reductions achieved from the divestment of carbon intense assets (thereby reallocating the emissions to another entity, rather than addressing the performance of the building itself). There is no requirement for organisations to disclose this carbon leakage, but it is encouraged that emissions reductions from this route are disclosed alongside a like-for-like approach to decarbonisation to make it clear how the entity is actually reducing emissions within their operations.

Entities that can demonstrate that their business model does not involve regularly buying/financing new buildings do not need to set an upfront embodied emissions target. While not currently defined, this may be complimented by the inclusion of a materiality threshold whereby exclusion of upfront carbon targets can be justified.

Implications

In-use Emissions

Figure 4: Financial Impact Assessment of Updated SBTi Approach

Based transition strategies and investment plans on the previous guidance issued by the SBTi, BIP.Verco have used our industry-leading Aim4Zero Model to map intervention requirements (and associated costs) against old and new SBTi approaches for a representative portfolio of European buildings (ca. 1,000,000 sqm):

Each coloured block represents the CAPEX requirements for a different set of carbon reduction measures1. From this exercise, it is apparent that a similar level of investment is required, under both scenarios, in the near-term (to 2035) but the updated pathway requires approximately 20% more capital allocation by 2050. Organisations must therefore act now to ensure that their strategies are sufficiently accounting for the long-term requirements of a 1.5°C aligned transition. This immediacy is echoed by the deviation in methodology from the SBTi away from an approach which accounts for higher emissions baselines, as organisations with higher baselines may have to focus on aligning their more carbon-intensive assets with the targets provided, rather than making more generalised portfolio-level reductions. Yet, it is currently unclear whether a shift in methodology will be required, should a portfolio be performing sufficiently that it’s reduction targets to align with CRREM are less than the ambitions outlined in the Corporate Standard.

Upfront Embodied Emissions

Beyond the investment requirements for addressing in-use emissions from energy consumption, the guidance notes that companies must use granular data from suppliers and value chain partners to calculate annual emissions. This is likely to be a departure for many companies who have historically used spend-based data to calculate embodied carbon emissions for Scope 3 reporting and target setting. The guidance also discourages the use of default datasets – commonly used in embodied carbon calculations, especially where product & supplier specific EPDs are unavailable, and for stages A4 & A5 where transport distances to site and material waste rates onsite frequently have to be estimated. This poses the question that in the case of limited resources, should the effort be spent collecting more accurate data for less material emission sources, or taking no-regret steps to actual decarbonisation?

The upfront carbon target pathways are also steep and will require significant planning and updates to practices, if they are to be achieved. Companies setting these targets are, to some extent, dependent on the upstream construction materials decarbonising and must therefore make tactical decisions in the procurement process, and exert pressure and influence on suppliers to enable this transition. This will also place greater challenges on developing countries with more carbon intensive supply chains and longer term growth projections; a reason that some form of location split in embodied carbon targets is essential.

BIP.Verco Takeaways

The SBTi Buildings Guidance, as it currently stands, provides the industry with some much needed clarification on the application of the GHG Protocol to the built environment. The targets developed are the most comprehensive that we have seen from a single standard, in their coverage and specificity. This embodies a convergence of market standards which rightly focuses attention on the most material emissions sources in the sector and the importance of taking immediate actions for their reduction. However, the nuances provided to the industry still leave too many questions unanswered, a significant gap in emissions coverage requirements (in-use embodied emissions, B1-B5), and an increase in the analytical burden on ESG teams and other stakeholders.

The fact that the SBTi are recognising carbon leakage is also a step in the right direction for the avoidance of doubt as to what classifies a robust reduction in emissions. However, the failure to make the reporting of these apparent emissions reductions mandatory increases the risk of greenwashing throughout the industry. The aim of the SBTi is, after all, to provide clear guidance on emissions reductions in line with a carbon constrained future, not to provide loopholes for exploitation through the tactical reallocation of capital.

The guidance also fails to provide any certainty to users on the point at which residual emissions may be neutralised to claim net zero status. While the efforts must be focused on actual emissions reduction, this lack of commercial end-goal may lead to challenges in onboarding certain key stakeholders and alienate those organisations more focused on maximising their financial returns.

The guidance papers and consultation response survey can be accessed here. BIP.Verco will be responding to the consultation to highlight the issues outlined in this article and share further views from our company’s experience. We encourage other real estate actors also to provide their feedback to ensure the robustness of the guidance, when it is released.

If you have any questions on the embodied carbon SBTi guidance, or more generally on low embodied carbon strategies, please contact Leah McCabe, Senior Consultant, Aim for Zero.

If you have any questions on the in-use SBTi guidance, or more generally on net zero frameworks, please contact Luke Riseborough, Consultant, Aim for Zero.