Setting robust science based targets has just become twice as hard – SBTI release new resources showing how 1.5°C is achieved

The Science-based Targets Initiative (SBTi) – the body which recognises corporate carbon targets as being consistent with climate science – has published a raft of new materials following a major overhaul of target setting pathways. This was driven principally by the IPCC special report on 1.5°C, published in October 2018.

For the first time, long-term targets must be consistent with the level of decarbonisation required to keep average global temperature rise to well below 2°C compared to pre-industrial temperatures, to be validated and recognized by the SBTi.

Among new materials is a new target-setting tool, which compares target commitments against key decarbonisation scenarios in both the Absolute Contraction Approach (ACA) and the Sectoral Decarbonisation Approach (SDA) – two common methodologies for setting science-based targets.

This tool also includes a new sheet to calculate targets aligned with the SBTI’s scope 3 criteria, something previously unavailable. This is accompanied by a v4.0 of the SBTi guidance document.

A sea change in corporate ambition

What do these new changes mean for business? For those that have already set targets in line with the old pathways, there will now be a need to check whether they meet the new requirements. Some may find they need to re-commit to more ambitious targets - carbon budgets are significantly more constrained in a ‘beyond 2 degrees’ world.

The SBTi manual employs different input climate scenarios depending on the SBT approach chosen. To take one example, under the SBTi’s 2°C Scenario (2DS), annual energy-related CO2 emissions are reduced by around two-thirds from today’s levels by 2060, permitting cumulative emissions (a total carbon budget) of around 1,170 GtCO2 between 2015 and 2100 (including industrial process emissions). By contrast, the Beyond 2°C Scenario (B2DS) has an equivalent carbon budget of 750 GtCO2 over the same period. This is consistent with a 50% chance of limiting average future temperature increases to 1.5°C. To give us a 67% chance of limiting warming to 1.5°C, the remaining budget drops to 570 GtCO2 – at our current rate of emissions we will exhaust this entire budget in just 12 years.

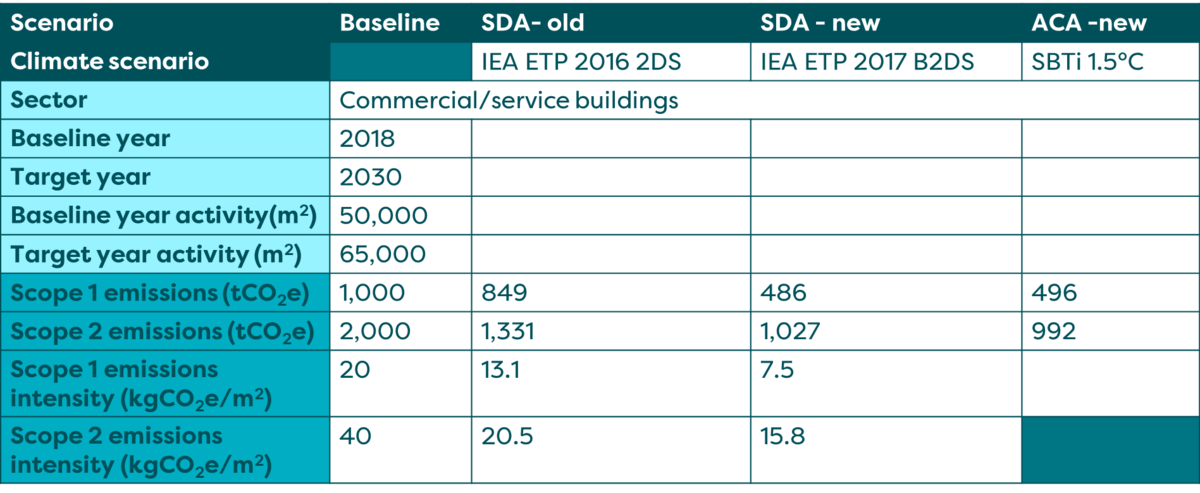

To compare the old with the new, we entered identical data for a fictional business into the previous and new SBTi pathway tools.

We chose a business operating in the commercial buildings sector of the Sectoral Decarbonisation Approach (1), with 50,000m2 of building floor area, and activities generating 1,000tCO2e of Scope 1 emissions and 2,000tCO2e of Scope 2 emissions in the baseline year of 2018. We anticipated a c.2% growth in floor area annually, taking the total floor area to around 65,000m2 by the target year for 2030.

The previous version of the pathway tool tells us that this business’s 2030 target would need to be at least a 44% reduction in total emissions intensity (kgCO2e/m2) by 2030, and an absolute reduction of 27%. More of this would be delivered in Scope 2 than Scope 1 (a 33% reduction in absolute Scope 2 emissions, compared with just 15% in Scope 1)(2).

The new pathway tool – which relies on the IEA’s ETP 2017 B2DS (Beyond 2 Degrees) scenario (3) - requires much greater ambition. For the same business, an SBTi-compliant 2030 target would need to be at least a 69% reduction in total emissions intensity (kgCO2e/m2) by 2030, and an absolute reduction of 50%. In this scenario the contributions from Scope 1 and Scope 2 area broadly similar on a percentage basis - a 51% reduction in Scope 1 absolute emissions and 49% reduction in Scope 2).

The new pathway is therefore roughly twice as ambitious.

Under the Absolute Contraction Approach (ACA), which takes any business's emissions to net zero by 2050 in a fairly simple, straight-line fashion, regardless of sector, the new pathway tool predicts a 30% reduction in Absolute Scope 1+2 emissions by 2030 for a 'well-below 2 degrees' target, and 50% for a 1.5 degree scenario. Due to the lack of 1.5°C scenario data from IEA, the SBTi currently does not provide an SDA option for 1.5°C targets, so businesses using this approach will only be able to develop 'well-below' 2 degrees targets.

Ringing the changes

The new SBTi criteria will be in effect as of 15th October 2019. All submissions received by the SBTi before this date can be assessed against version 3.0 or 4.0. For those already in the process of developing targets, the timing will be critical. Will they want to release targets into the public domain knowing that they may no longer be acceptable to the SBTi in 6 months’ time?

At BIP.Verco we welcome the fact that the SBTi have moved swiftly to align their criteria with the latest climate science. In our ‘Climate Coin Toss’ animation last summer we raised our concerns on the previous decarbonisation pathways, which only provided a 50% chance of avoiding 2°C warming. We see this as a major ‘raising of the bar’ and a key step in motivating more businesses to come out in support of net zero targets. We look forward to seeing the corporate response to these changes and the new cohort of business leaders that emerge. Indeed we predict a further ramping up of ambition with net zero ambitions becoming the new norm.

One other change applicants should be aware of is the charge for the SBTi’s validation service, which became mandatory earlier this year. The target validation service costs $4,950 (+ applicable VAT). This includes up to two target assessments (companies can choose either one preliminary and one official, or two official validations). Subsequent resubmissions cost $2,490 (+ applicable VAT) each.

If you need help in understanding what the revised SBTI criteria mean for your carbon targets, or would like to develop new SBTs in line with the latest climate science, please contact Paul Stepan, BIP.Verco’s Head of Policy, Strategy and Compliance (paul.stepan@vercoglobal.com).