How do offsets fit into a real estate net zero strategy?

As more real estate companies set Net Zero Pathways, it is now time to delve deeper into understanding how offsetting and carbon pricing fit into this strategy and how much they can be relied on to achieve carbon targets.

Offsets remain a hotly debated and controversial topic, particularly in the wake of the recent wave of organisations making zero carbon commitments, and the potential over reliance of many companies on purchasing carbon credits to achieve these claims. As well as concerns around the integrity of offsets, there is a challenge due to the scale of global emissions produced (and forecast) compared to the potential to scale offsetting options. In reality, this means net zero cannot be achieved solely through offsets and a reduction in emissions is required. In real estate the energy hierarchy is considered best practice with offsetting as the last resort, a necessary final step to help organisations achieve their net zero ambitions.

This article will provide an introduction to common questions regarding offsetting in the real estate sector. For more bespoke and in-depth support please contact the BIP.Verco team to find out how we can help advise on offsetting as part of your Net Zero Pathway.

Can I use offsets for all emissions to claim Net Zero?

Zero Carbon Definitions

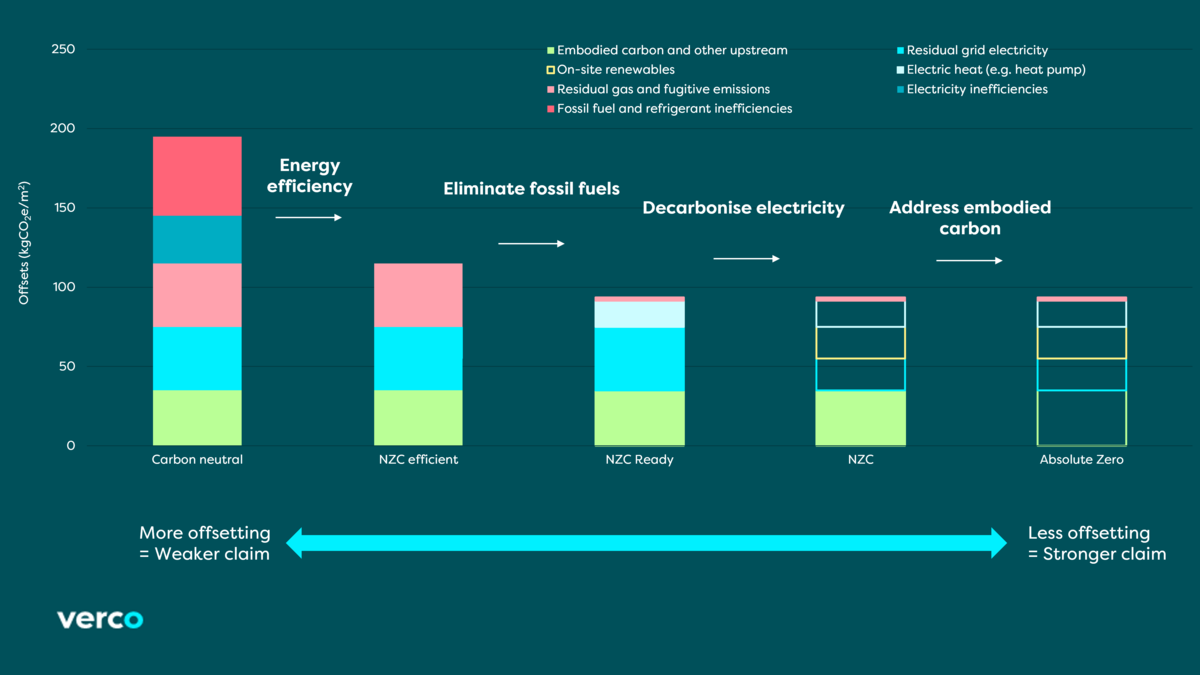

The answer to this lies in understanding the differences between the various building-level ‘zero carbon’ definitions. The visual below, produced by BIP.Verco for the Investment Property Forum’s (IPF) research into pathways to Net Zero Carbon Emissions in International Real Estate Investment, explores the relationship between different ‘zero carbon’ terms (1).

Strictly speaking, if offsets are purchased for all emissions, a company could claim to be ‘carbon neutral’ but a strategy along these terms goes very little way to achieving meaningful action towards addressing climate change and companies satisfied with using offsets in lieu of achieving actual reductions of emissions may find themselves target to ’greenwashing’ criticism.

In order to achieve the more ambitious claim of ‘net zero’, buildings must prioritise energy efficiency, removal of fossil fuels and ensure all remaining demand is met by electricity sourced from renewable energy. A climate leader would aim to achieve absolute zero, however in real estate some emissions are particularly challenging to decarbonise, such as the embodied carbon of built materials and refrigerants. Thus, limited offsets are still required until technology or innovation evolves to achieve absolute zero.

Rules for specific Net Zero claims

While the definition of ‘net zero’ broadly follows these general principles of the energy hierarchy, more detailed rules around the amount of offsetting allowed in a net zero claim vary between frameworks, so organisations should ensure their strategy is in line with specific schemes or initiatives they are signed up to or claiming against.

For example, the Science Based Target initiative (SBTi) does not permit the use of offsets for near-term targets. For long-term targets, companies are typically required to reduce their emissions by 90% across all scopes and limits the use of offsets to only the residual emissions making up no more than 10% within the Corporate Net Zero Standard (2).

How do I choose the right offsets?

In the real estate sector, considerable work has already been undertaken to help define criteria for choosing high-quality offsets. In the UK, the two most often referenced guides are the UKGBC Renewable Energy Procurement and Carbon Offsetting framework (3) and the UK Oxford Offsetting Principles (4). Credible offsetting strategies should align with the criteria set out by the UKGBC, and companies making net zero building claims should disclose the number and type with a link to the relevant crediting mechanism registry entry and, for best practice, the price paid for offsets used. The UKGBC’s proposed offsetting criteria mirror those of most crediting mechanisms, in that credits must be:

1. Real

2. Avoid leakage – i.e. emissions are not truly reduced, but just displaced elsewhere.

3. Measurable

4. Permanent

5. Additional

6. Independently verified

7. Unique

8. Avoid social and environmental harms

To ensure these criteria are met, it is recommended to purchase credits through so called ‘high quality’ crediting mechanisms, such as those listed by the International Civil Aviation Organisation for the International Aviation carbon offsetting scheme which has a degree of independent quality oversight over permissible credits (5).

The Taskforce on Scaling Voluntary Carbon Markets last year announced the formation of an Integrity Council for Voluntary Carbon Markets (IC-VCM), following a shift in focus from scaling up the carbon market to focusing on ‘high-quality, transparent and consistent meta-standards’. The IC-VCM is due to release their Core Carbon Principles (CCP) in Q3 2022, which are designed to set a global standard for carbon credits (6).

How does offsetting fit into a real estate Net Zero Strategy?

Once organisations have calculated their total footprint and prioritised reductions of direct and indirect emissions, they may then choose to include an offsetting strategy as part of their overall net zero approach. This is an area we are seeing a number of investment managers looking to develop now, and making this adaptable, simple to follow and aligned with house level strategy is an evolving topic.

Some organisations may consider splitting their funds, so those more ambitious adopt a strategy to become net zero earlier and factor offsetting into strategy and operations from the outset. For remaining funds, their remaining emissions would be offset in line with the overall net zero target date. Another consideration could be to offset specific scopes (landlord vs tenant or operational vs whole building) as a priority in tandem with reducing the emissions from these areas. A decentralised approach can give funds the opportunity to choose offsets matching their own values or local to their portfolio, but it can also raise challenges in managing the quality of offsets and accurately disclosing. Identifying reasons for offsets will help guide how many and which type of offsets are required.

At either a fund or organisational level, offsetting strategies may be developed as a unique feature for a company and allow focus on achieving local or social impacts that tie in with CSR or a broader ESG agenda.

A constraint regarding the choice of offsets will ultimately come down to cost, balancing wanting to do what’s best and achieving multiple benefits and what is commercially viable. While pricing of offsets is often opaque, in principle higher quality offsets providing multiple additional benefits will be more expensive that those with limit additionality (e.g. supporting already commercially-viable renewable energy projects). With a fiduciary duty to deliver commercial returns for investors, fund managers may need to find ways to recognise the value of higher quality offsets with multiple benefits, such as internalising social costs in order to balance with the overall fund’s strategy.

How do I adopt a leadership or best practice approach?

Offset Strategy

Based on the latest analysis by the Climate Action Tracker, with all current policy globally, the world is still on track for +2.7oC temperature increase (7). This reduces to +2.1oC if all long term and net-zero targets are also achieved. With this in mind, there is significant compelling sustainable, not to mention competitive and reputational justification to be more ambitious than is necessary to achieve net zero.

In addition to any required offsets, companies are encouraged to mitigate activities above and beyond their value chain. This is recommended by the SBTi as it recognises the scale of the challenge in limiting warming to 1.5oC and identifies this as an additional action to help keep this ambition possible (8).

Another avenue many organisations are considering is to develop a transition fund. This approach effectively internalises the currently unaccounted cost of environmental damage of carbon emissions. The company sets an internal carbon price, aligned with best practice recommendations that reflect actual carbon value. This is applied to all residual emissions within scope to calculate the total transition fund. The residual carbon emissions are offset through approved standards previously discussed, and the remainder of the transition fund is spent on supporting projects of the organisations choosing. These additional projects are subject to less stringent rules than the formal offsets and allow a fund to invest in technologies that may benefit their specific assets or geographies in the future.

Offset Types

The majority of current offsets issued are carbon reductions, made up predominantly of forestry and land use projects, followed by renewable energy (9). While preserving existing ecosystems is essential for the protection of carbon stored, and conservation of biodiversity, these nature-based solutions are not sufficient to achieve net zero.

Two anticipated key transitions, highlighted in the Oxford Offsetting Principles, are the shift to carbon removals as opposed to carbon reductions, and the shift to long-lived storage. Permanent carbon removals (neutralisation), which can take place within or outside a company’s value chain, are not yet available at scale. However, a number of frameworks restrict offsets to permanent carbon removals as part of a net zero claim, including the Net Zero Asset Managers Commitment (10) and the SBTi (11).

Therefore, within their offsetting strategy, companies should consider whether early adoption of neutralisation options is preferable to signal increased demand within the market. Or alternatively, companies may want to set staggered offset type targets along the journey to net zero balancing the relative benefits for each offsetting type.

Included in the Oxford Offsetting Principles is the recommendation to revise offsetting strategy as best practice evolves. This is a key message as the requirements, regulations and expectations around offsetting are expected to evolve in the coming years.

Should an internal carbon price be set?

There are two main figures to consider with carbon pricing; the cost of current and predicted future credits and the price of carbon that reflects it’s true economic and societal impact.

Voluntary carbon credit prices

Prices of voluntary carbon credits vary significantly, but the vast majority currently sit well below all other carbon price references, such as compliance markets, taxes and suggested shadow prices. Typical voluntary credit prices currently range from about £1-5/ tCO2e for high volume / forestry projects, to £5-20/ tCO2e for small volume and higher quality credits. The price of carbon credits are expected to rise substantially, with some estimates looking at an increase to £40* by 2030 and to £80* by 2050 (12), with other estimates even higher.

This increase is driven both by the growth of the market as more companies rely on offsets to meet their targets, as well as an expected shift in offset types. Long lived carbon removals with a larger reliance on new and evolving technologies will be more expensive compared to current carbon reductions with short-lived storage.

Recommended carbon value

In response to the fact that current voluntary carbon credits prices are far lower than the cost of carbon needed to achieve Paris goals, organisations are encouraged to set an internal carbon price on whole life carbon that reflects it’s true value. This can then be used to drive decision making, prioritise low carbon investment and change internal behaviour.

The UKGBC recommends setting a carbon price aligned to the Paris Agreement and references a minimum value of £70/tCO2 based on the UK 2020 HM Treasury Green Book non-traded central scenario (13). The UK Green Book has since been updated and new values for carbon, published in 2022, have increased to £245/tCO2 for 2021, reflecting the relatively high cost of carbon removals in the UK, reliant as we are on technical solutions for the volume required (14). Valuations for carbon vary, with some international studies suggesting around £80 - £112/ tCO2* by 2030 to be consistent with less than 2oC warming (15)(16). Therefore a regular review of carbon valuations, and consideration of the scope of GHG emissions that the price applies to, is recommended for internal price setting (17).

Watch webinar: Internal carbon pricing explained

Conclusion

As a key part of real estate's net zero strategy, an organisation’s response to offsetting is dependent on stakeholder expectation but can also provide an opportunity to prepare for a carbon constrained world. This article has provided an introduction to some of the key themes to consider around offsets in a Net Zero strategy.

For more information, or to find out how BIP.Verco can assist you in setting or understanding how offsetting can fit into your Net Zero strategy, please get in contact.

*Costs converted to sterling from US dollars for comparison in this article