ISO 14060: Corporate net zero becomes auditable

On 17 June 2026, the International Organisation for Standardisation opened a public consultation on ISO 14060, its draft Net Zero Standard for organisations. It arrived six days after the SBTi published Version 2.0 of its Corporate Net-Zero Standard, and it sits on top of a greenhouse gas accounting layer that is still being finalised.

If you’re already familiar with the SBTi, the question is whether this a big deal, a small deal, or something to worry about now.

Nothing is mandatory yet, so there is nothing to comply with. But ISO 14060 changes what a credible net zero claim has to have to survive, and a few of its rules have financial implications if your decarbonisation plan quietly assumes otherwise.

What is ISO 14060?

ISO14060 sets out what an organisation has to do to make a net zero claim that an accredited third party can check. It is not a new way to count emissions. It builds on the accounting you already use, the GHG Protocol and ISO 14064-1, and puts a governance framework on top.

It turns ISO’s Net Zero Guidelines (IWA 42:2022), which were non-binding advice, into a formal standard that can be validated, verified and, in time, written into regulation.

It applies to organisations, not to products, services, brands or territories, and it was built primarily for non-financial institutions. Financing and investment activity is routed to a separate standard (ISO/FDIS 32212), so a financial institution can apply ISO 14060 to its own operations but not to its portfolio.

Key takeaways

This is a proposed governance and assurance standard, not a new carbon accounting, or a management standard (such as ISO50001 for energy efficiency). Your inventory method does not change.

Net zero claims are proposed in four stages, each independently validated. You report progress along the way, not only at the finish line.

Targets are proposed to be set separately for Scope 1, 2 and 3. Scope 1 is a hard cumulative budget. Miss a Scope 2 or 3 target and you get a defined grace period, but you pay to cover the gap.

Near-term target achievement is proposed to relate solely to physical GHG emissions, without the variety of consequential (impact) accounting and alignment target options of SBTI v2.0.

The 2020 base year is a proposed global pathway anchor, not a requirement to baseline your own operations on a pandemic year. The rule is that a later start does not buy a lighter carbon budget.

It is proposed that removals used at net zero must be durable for at least 100 years. Cheap nature-based credits will not counterbalance your residual emissions.

Consultation closes on 17 August 2026. Publication is expected around May 2027.

The four claims

ISO 14060 lets you make a verifiable claim at each stage of maturity, rather than withholding recognition for decades:

Net zero aspiration

You have committed, and you are building the inventory and a costed transition plan.Net zero aligned transition plan

The plan is finalised and built into business strategy and budgeting, not a standalone sustainability document.Net zero aligned progress

You are delivering against interim targets and cumulative budgets, or you are in a documented catch-up period.Net zero achievement

Deep reductions down to a minimal residual, with that residual counterbalanced by durable removals.

You cannot skip stages, and each one is checked.

The 2020 base year

There might be a worry upon first read that ISO forces a 2020 base year, and that 2020 is a bad choice because it was a pandemic year with abnormal operations. That conflates two different things.

2020 is the anchor for the global pathway and carbon budget, drawn from the IEA and IPCC scenarios that model immediate global action from 2020 onwards. It is not a requirement to baseline your own inventory on 2020 numbers. You can select a later base year for your own operations, but the cumulative global emissions since 2020 are subtracted from the budget underlying your pathway. A later start does not buy a larger budget.

So the issue is not pandemic distortion in your baseline. It is that the standard makes you carry the historical debt either way.

What does an ISO target look like?

If you hold an SBT, you are used to a percentage to hit by a target year. ISO works differently. It’s binding requirement is that your emissions, added up across every year from 2020 to net zero, stay within a cumulative carbon budget drawn from a peer-reviewed, Paris-aligned pathway. The destination is broadly the same, a roughly 90% cut by 2050, but the test is the running total rather than the endpoint. Every year counts, and a tonne you do not cut early is gone from the budget.

How you arrive at the budget is open. The standard offers its own worked method, built on sector and country budget factors, and the figures below come from this. But these factors sit in its informative annexes, which are guidance rather than requirements. ISO expressly let you use any peer-reviewed method that produces similar or lower cumulative emissions. For many companies that means an existing SBTi pathway, which is already peer-reviewed and 1.5°C-aligned, can serve as the basis, as long as its cumulative emissions are no higher.

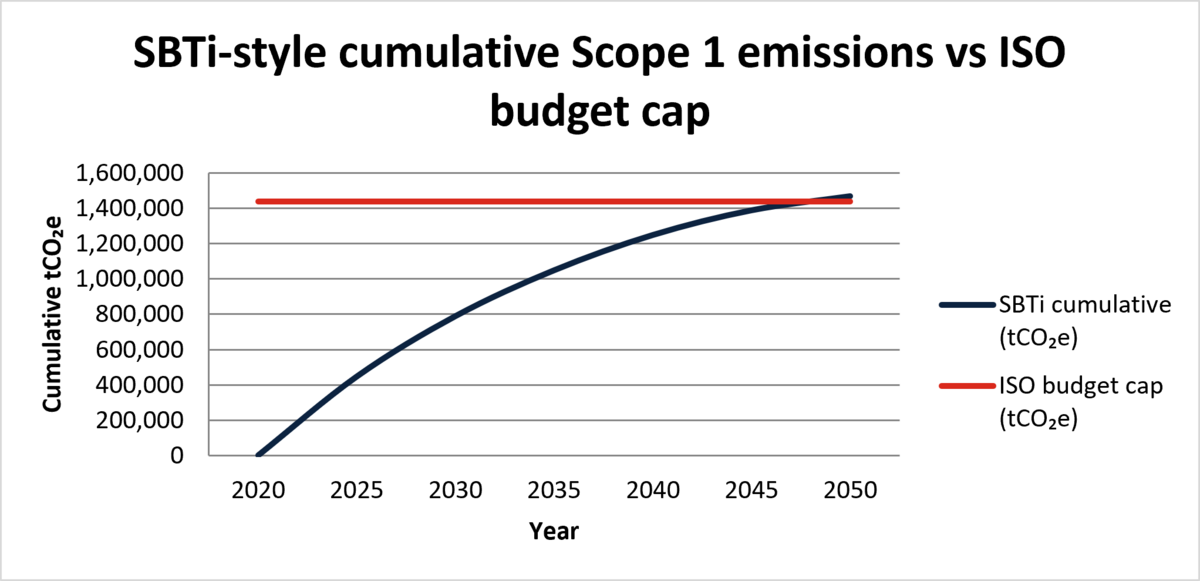

Scope 1 is the hard line. You set a cumulative budget for direct emissions and stay within it. There is no grace period. Overshoot the budget and you lose your progress claim until you bring direct emissions back within it. On the standard’s worked method the budget is a single factor times your 2020 emissions, about 14 times base-year emissions from a typical 2050-country company across the whole period to net zero.

Scope 2 is where ISO and SBTi diverge most. SBTi lets PPAs and energy certificates count toward the target. ISO sets the long-term Scope 2 target to be set on a location-based basis, and the interim targets expressed as the share of low-carbon energy you consume, where certificates and PPAs may count. So your Scope 2 falls as the grid decarbonises and as you actually consume clean power, not as you buy certificates. If you put a budget on it, the worked method uses the power-sector pathway, the fastest-decarbonising in the standard is about 10 time a base-year emissions, or a national grid pathway.

Scope 3 uses the same budget logic, built up across the value chain. You split it by sector and combine the pathways, or use an all-sector figure for a complex chain, again about 14 on the worked method. You set targets on every significant category, judged by magnitude and influence, and publicly justify anything you leave out, with activity targets such as supplier engagement, energy efficiency and no deforestation alongside.

Scope 2 and 3 carry a flexibility Scope 1 does not. Miss an interim Scope 2 or 3 target by up to 25% and you keep your claim, with up to three years to recover, as long as you finance the shortfall and disclose it. Miss by more than that, or breach Scope 1, and the claim falls away. For Scope 3, the most volatile part of any inventory (a fixed 25% threshold with a financed catch-up) is arguably easier to defend than a best-efforts approach. It is a number you can document, not a judgement about whether you tried hard enough.

More on Scope 1 target setting (optional addition)

On the standard’s worked method, the budget factor is best read as the number of years of base-year emissions you may emit in total, from 2020 to your net-zero year, not each year. It is about 14 for a typical 2050-country company, tighter for fast-decarbonising sectors, around 10 for power, and looser for hard-to-abate ones, around 18 for heavy industry and 27 for aviation. A higher-income country gets a smaller budget for the same activity, because it reaches net zero earlier.

So, a company emitting 100,000 tonnes of Scope 1 in 2020 has a budget of about 1.44 million tonnes to net zero. Interim targets still come out as familiar annual reductions, but they are carved out of that total. These figures are the standard’s illustration on one acceptable method, not a fixed rule. Another peer-reviewed method that gives similar or lower cumulative emission is equally valid. The catch for an existing SBT holder is that ISO counts every tonne from 2020, so the emissions you have produced since then are already drawn down from the budget.

One caution. The certificates and contracts behind Scope 2 and 3 sit in a part of the GHG Protocol that is being rewritten. ISO ring-fences them (clause 11.2), accounted separately from your physical inventory, tied to an equivalent volume of your own emissions, and never a substitute for real cuts. But it defers the detailed accounting to the GHG Protocol's Actions and Market Instruments rules, which are not expected before the end of 2028. If your Scope 2 or 3 plan leans on them, treat how they are counted as provisional.

Removals

To counterbalance residual emissions at net zero, ISO 14060 requires carbon removals expected to last at least 100 years. Reduction and avoidance credits do not count.

That converts a soft assumption into a hard liability. If your long-term plan leans on cheap nature-based offsetting to mop up residuals at 2050, ISO breaks that assumption and pushes you toward durable, engineered and geological storage, the scarcest and most expensive supply today. Price that liability now, on durable-removal costs. It materially changes the cost of the finish line, and it is better found in a model than in a boardroom in 2049.

Does this replace SBTi? No.

Read the two June releases together and the division of labour is clear:

- SBTi remains the voluntary, high-visibility investor signal.

- ISO is the formal standard that an accredited body can certify and a regulator could reference under regimes such as CSRD and IFRS S2.

There is an overlap - a company engaged in the SBTi Corporate Net Zero Standard should have little trouble making ISO 14060 accredited claims.

What to do now

Nothing here requires compliance, because there is nothing yet to comply with, and the ISO net zero standard is just in consultation. The immediate recommended actions are:

Read the standard here.

Test the logic of your current target architecture and decarbonisation plan against the logic of the ISO's rules.

File consultation comments where the draft creates real operational / financial impact for you. It closes on 17 August 2026.

To discuss what ISO 14060 means for your targets, or for a portfolio, contact our team.

Experts on the topic