SFDR 2.0: What asset managers and institutional investors need to know

The European Commission proposed a review of the Sustainable Finance Disclosure Regulation (SFDR) in November 2025. In light of this, Senior Consultant Mariya Chervonogradska shares the latest insights on the proposed SFDR 2.0 regulation and what it could mean for asset managers and institutional investors.

What is the SFDR?

The Sustainable Finance Disclosure Regulation (SFDR) entered into force in March 2021 as a cornerstone of the EU Sustainable Finance Action Plan, supporting the EU’s climate action goals.

Its original objective was to enhance transparency by requiring financial market participants and advisers to disclose how they consider sustainability risks, principal adverse impacts, and sustainability-related claims in their investment processes and products.

Since March 2021, the SFDR has reshaped EU finance, notably driving capital towards products marketed as sustainable. However, its use of Articles 6, 8, and 9 as de facto labels, rather than disclosure tools, led to market inconsistencies, high costs, and greenwashing concerns. This prompted the current review.

What is the SFDR 2.0?

To address the shortcomings identified in the current framework. and to simplify and strengthen the EU sustainable finance regime, the European Commission proposed a comprehensive review of the SFDR in November 2025. This is commonly referred to as the SFDR 2.0.

The review aims to reposition the SFDR from a complex and often misunderstood disclosure regime into a clearer, more investor-oriented framework, while preserving high standards of sustainability transparency and market integrity.

At its core, the SFDR 2.0 seeks to:

- improve clarity and usability for investors;

- reduce regulatory complexity and compliance burdens;

- address greenwashing risks more effectively; and

- align more closely with other key EU frameworks, including the EU Taxonomy, the Corporate Sustainability Reporting Directive (CSRD), and EU Climate Benchmarks.

What are the proposed changes?

The proposal introduces structural reforms, such as shifting Articles 6, 8, and 9 from labels to clear, voluntary categories ('Sustainable,' 'Transition,' and 'ESG Basics'). It mandates stricter rules for non-categorised products and strengthens alignment with the EU Taxonomy and Climate Benchmarks.

Overall, the proposal marks a shift from disclosure-led compliance toward a classification system based on defined criteria and performance. Notably, the introduction of a Transition category is intended to better accommodate investment strategies that support credible decarbonisation pathways, while avoiding the binary distinction between “sustainable” and “non-sustainable” products.

This fundamental change from an article-based system to a criteria-based system means asset managers will be forced to conduct a strategic re-evaluation. It is likely that they will need to reclassify their entire existing product range, particularly the funds currently marketed under Articles 8 and 9. This represents a major operational challenge, as it requires robust data, revised investment strategies, and a significant communications effort to manage client and investor expectations during the transition.

The scope and target audience of SFDR 2.0

Under the proposed changes, the SFDR will continue to apply to financial market participants who manufacture or manage financial products. The scope includes asset managers, financial product manufacturers and alternative investment fund managers.

Pure financial advisers, while removed from the SFDR's direct scope, remain subject to sustainability rules under existing sectoral legislation like MiFID II.

Expanding the scope to retail investors significantly raises the stakes for product claims. Marketing materials and product names for categorised funds will face scrutiny from a less financially sophisticated but far more numerous investor base, along with their advocates and national regulators. This increases legal and reputational liability; claims must not only be accurate but also clear and fair to avoid accusations of greenwashing from a sensitive public audience. Effective communication and robust substantiation of sustainability credentials will become critical commercial imperatives, not just compliance exercises.

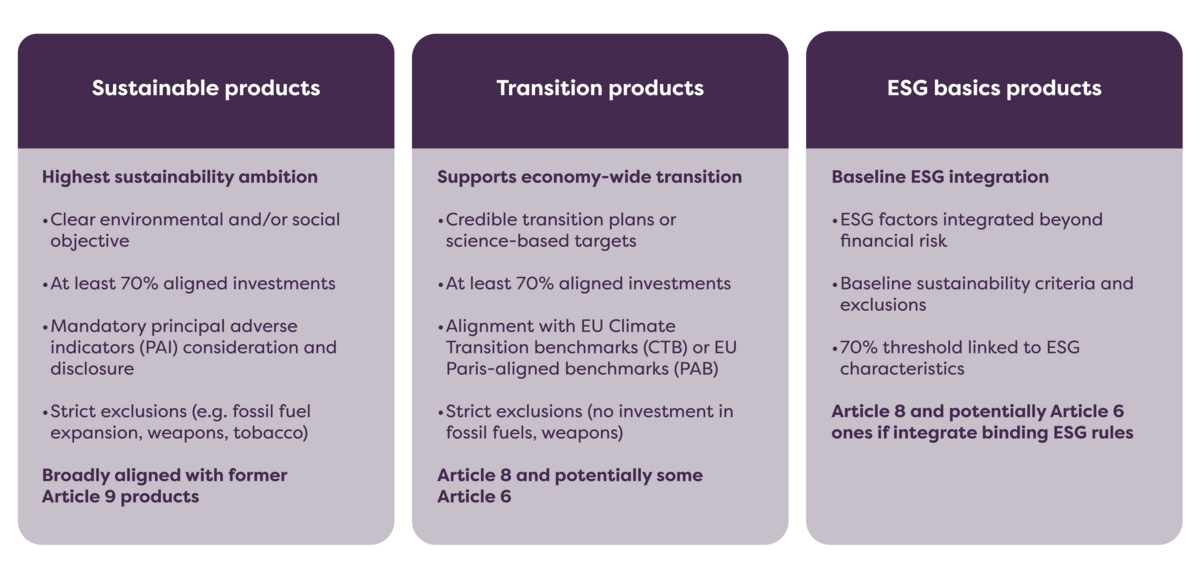

Suggested categories

The SFDR 2.0 introduces three voluntary sustainability-related product categories, along with their minimum criteria, thresholds and disclosure requirements:

Products that do not meet these criteria fall outside the categorisation regime and face stricter rules on sustainability-related claims.

Non-categorised products

Products that do not meet the criteria for any of the three categories:

- cannot use sustainability-related terms such as “sustainable”, “green”, “ESG” or “impact” in their names or marketing materials; and

- must rely on strictly factual disclosures without sustainability positioning.

This change is central to the Commission’s effort to curb greenwashing and improve market discipline. Consequently, the decision to not pursue a sustainability category under the SFDR 2.0 must be an active, strategic one. Managers must weigh the cost and effort of categorisation against the significant risk of their product becoming isolated in a market that is progressively rewarding transparent sustainability credentials.

Link with the EU Taxonomy

The SFDR 2.0 strengthens the link with the EU Taxonomy, particularly for products in the Sustainable and Transition categories that pursue environmental objectives.

For these products:

- disclosure of Taxonomy alignment becomes mandatory; and

- the Taxonomy serves as a key reference point for defining environmental sustainability.

This mandatory disclosure transforms the EU Taxonomy alignment percentage into a direct, comparable performance indicator for investment products. Investors will use these standardised figures to benchmark and select funds, making Taxonomy alignment a core component of competitive positioning and product due diligence in the sustainable finance market.

Link with funds following EU Climate Benchmarks

Products that track or reference EU Climate Transition Benchmarks or Paris-Aligned Benchmarks benefit from regulatory recognition under the SFDR 2.0.

Such products meet several of the minimum criteria for the Transition category, reinforcing alignment between benchmark regulation and product sustainability disclosures.

Implications for investors

Although the SFDR 2.0 proposal does not yet define detailed thresholds, metrics, or reporting rules, it establishes clear principles and requirements for the new product categories, providing a framework that guides asset managers and institutional investors in structuring and disclosing sustainability-related activities.

For investors and managers, the SFDR 2.0 promises greater clarity and comparability, potentially lowering long-term compliance costs but demanding immediate strategic action. The imperative will be to reassess product ranges, fortify ESG data, and prepare for recategorisation to mitigate legal, reputational, and commercial risks.

When will the SFDR 2.0 apply?

The proposal is currently subject to negotiation between the European Parliament and the Council.

While timelines remain indicative, adoption is expected within the next legislative cycle, followed by:

- a transitional period; and

- the development of revised Level 2 measures.

While the final detailed rules will follow later, this timeline makes proactive preparation strategically important. A pragmatic preparation roadmap should include:

- 2026 (pre-finalisation) - Conduct a comprehensive gap analysis. Audit existing product portfolios against the proposed category criteria and strengthen ESG data governance to meet future threshold requirements.

- 2027 onwards (implementation and transition) - Execute reclassification, align reporting systems with final Level 2 standards, and manage client communications.

Beginning this structured preparation now will help with a smooth transition. It will also help your firm to maintain a competitive advantage as the rules solidify.

How to prepare

Firms should immediately begin mapping products to proposed categories, reviewing sustainability thresholds, and strengthening data capabilities to ensure disclosures align with both the Taxonomy and CSRD.

How we can support you

Successfully navigating the transition to the SFDR 2.0 will require strategic planning and operational change. As firms begin their preparation, several critical considerations emerge:

1. Strategic product positioning

The shift to new categories requires a fundamental review of fund objectives and market positioning. Firms must decide which category aligns with each product's true strategy and investor expectations, avoiding both category stretching and the commercial risk of being non-categorised.

2. Data governance and gap analysis

Robust, auditable ESG and climate data is key. The criteria for the 'Sustainable' and 'Transition' categories requires precise metrics and evidence. Firms should immediately audit their data gaps, governance, and sourcing capabilities against the proposed requirements.

3. Transition plans and roadmaps

It’s crucial, at this stage, to develop credible transition plans and set science-based targets.

4. Disclosures

Firms will need to update their prospectus, periodic, and website disclosures to clearly reflect the new categories and requirements. Early preparation of standardised templates will help ensure consistency, support regulatory expectations, and reduce the risk of misalignment as the rules are finalised.

5. Formal ESG data assurance

External assurance enhances the confidence of decision makers in the accuracy, reliability, and credibility of ESG data disclosures.

Given this complexity and the strategic stakes, many firms will benefit from external expertise. Specialist support can be invaluable for tasks such as conducting a 'shadow categorisation' of existing portfolios, developing science-based transition roadmaps, performing gap analyses against upcoming criteria, and aligning reporting frameworks with the evolving regulatory landscape.

With experience in net-zero audits, EU Taxonomy alignment, the development of due diligence tools for investment risk screening, and climate resilience assessments, our team of experts can equip asset managers and investors to approach SFDR 2.0 with confidence and clarity.

Please get in touch to find out how we can help you.

Experts on the topic: